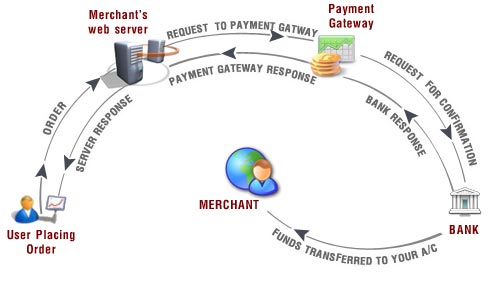

The first thing you need to know about is discount rates. These rates (usually 2-6%) are commissions split by a few parties taken from your client’s payment. They are attributed to your merchant account provider and/or payment gateway and finally, the credit card provider. They will vary greatly depending on the payment gateway/ merchant account setup you choose but will be involved in any credit card transaction you ever make.

With some payment gateways, the discount rate will decrease as the your total monthly sales amount is increased through that gateway. For example, with Google Checkout, the discount rate a totally monthly sales of less than $3000 will be 2.9% but for over $10,000, it would decrease to 2.2%.

Monthly Fees

Almost all payment gateways that require a merchant account charge a monthly fee. The more services and functions your gateway offers (or you choose), the higher these fees will be.

It’s worth noting that some of these fees are optional, and if you integrate with an application to handle your e-commerce, you may not need some options. For example, some payment gateways will add an extra charge if you want to use their service to enable auto-billing (the ability to process regular, pre-authorized payments on a client’s credit card). If you set up auto-billing in ECPSS merchant account , you don’t need to pay anything extra to your payment gateway.

One common value-added feature you might want to consider is a fraud detection toolbox. With most payment gateways, you are given a number of tools to help you guard against fraud, such as filters to define the scope of people or places you receive payments from. As an example, ECPSS payment offers their Advanced Fraud Detection Suite. It’s a good idea to add this service if you will be accepting payments from people who you do not have an existing relationship with (ie people who sign up on your website, as opposed having been a client for 10 years) because it will help reduce chargebacks.

Per Transaction Fees

Lastly, for each transaction you process, most payment gateways charge a flat fee. It’s usually under fifty cents per transaction, but I’m afraid this fee is pretty much unavoidable.

Setup Fee

When you sign up for a payment gateway, there is also usually a setup fee. Sometimes, it’s free (like PayPal Standard), but most of the time the setup fee ranges from $49 – $250. The good news = at least the setup fee is only a one-time charge, and I am positive you will quickly earn it back.

Laid out like this all in one list, the costs may seem surprising. But when you factor the costs into enhanced convenience for your customers and dramatically improved cashflow, as well as the time your will save collecting from your customers (no checks in the mail, or records to update because ECPSS payment gateway will do that automatically), it is well worth it.